All Categories

Featured

Table of Contents

The strategy has its very own advantages, however it additionally has concerns with high charges, intricacy, and much more, leading to it being considered as a scam by some. Boundless financial is not the best policy if you need just the investment element. The limitless banking principle focuses on the usage of whole life insurance policy policies as an economic device.

A PUAR enables you to "overfund" your insurance plan right approximately line of it coming to be a Changed Endowment Agreement (MEC). When you make use of a PUAR, you quickly increase your cash worth (and your death benefit), therefore increasing the power of your "bank". Better, the more cash money value you have, the better your interest and returns payments from your insurer will be.

With the surge of TikTok as an information-sharing platform, financial suggestions and methods have discovered an unique method of spreading. One such approach that has been making the rounds is the limitless financial idea, or IBC for short, amassing endorsements from stars like rapper Waka Flocka Fire - Cash flow banking. Nevertheless, while the approach is currently preferred, its roots map back to the 1980s when economist Nelson Nash introduced it to the globe.

What are the tax advantages of Policy Loan Strategy?

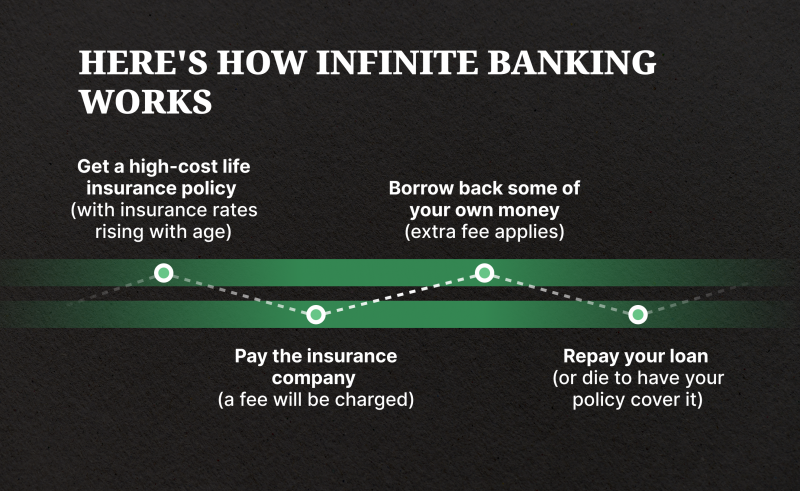

Within these policies, the cash value expands based upon a price established by the insurance firm. When a considerable cash value builds up, insurance holders can get a cash worth lending. These finances differ from traditional ones, with life insurance policy serving as collateral, implying one can shed their insurance coverage if borrowing excessively without sufficient cash worth to support the insurance policy expenses.

And while the appeal of these plans appears, there are inherent limitations and dangers, necessitating thorough money worth tracking. The strategy's legitimacy isn't black and white. For high-net-worth individuals or company owner, specifically those utilizing approaches like company-owned life insurance policy (COLI), the advantages of tax breaks and compound development can be appealing.

The allure of unlimited financial does not negate its obstacles: Expense: The foundational requirement, a long-term life insurance policy policy, is more expensive than its term counterparts. Qualification: Not everybody receives whole life insurance policy because of strenuous underwriting procedures that can omit those with particular wellness or lifestyle conditions. Complexity and danger: The elaborate nature of IBC, combined with its risks, may prevent many, especially when simpler and much less dangerous choices are available.

What makes Leverage Life Insurance different from other wealth strategies?

Designating around 10% of your regular monthly revenue to the plan is just not possible for lots of people. Utilizing life insurance policy as an investment and liquidity source requires self-control and tracking of plan cash money worth. Seek advice from an economic expert to determine if boundless financial aligns with your concerns. Component of what you read below is merely a reiteration of what has actually already been said over.

So prior to you obtain on your own right into a circumstance you're not gotten ready for, recognize the following initially: Although the idea is frequently offered thus, you're not really taking a funding from on your own. If that were the instance, you wouldn't need to repay it. Instead, you're obtaining from the insurance policy firm and need to repay it with passion.

Some social media posts suggest making use of money worth from whole life insurance policy to pay down credit report card financial debt. When you pay back the funding, a part of that passion goes to the insurance company.

What are the risks of using Whole Life For Infinite Banking?

For the first numerous years, you'll be settling the commission. This makes it incredibly tough for your plan to gather worth during this moment. Entire life insurance expenses 5 to 15 times extra than term insurance. Many people simply can not afford it. So, unless you can afford to pay a few to a number of hundred bucks for the next decade or more, IBC won't benefit you.

If you call for life insurance policy, right here are some useful suggestions to consider: Consider term life insurance coverage. Make sure to go shopping about for the finest price.

How flexible is Infinite Banking Benefits compared to traditional banking?

Visualize never ever needing to stress over small business loan or high passion prices once again. What if you could obtain cash on your terms and build riches simultaneously? That's the power of unlimited banking life insurance policy. By leveraging the money worth of whole life insurance coverage IUL policies, you can expand your wealth and borrow money without depending on conventional financial institutions.

There's no collection financing term, and you have the liberty to pick the settlement timetable, which can be as leisurely as repaying the loan at the time of death. This flexibility encompasses the servicing of the financings, where you can go with interest-only payments, keeping the loan equilibrium level and manageable.

How do interest rates affect Policy Loans?

Holding cash in an IUL taken care of account being attributed interest can frequently be much better than holding the cash on down payment at a bank.: You've constantly desired for opening your very own pastry shop. You can borrow from your IUL plan to cover the initial expenditures of renting a space, acquiring tools, and employing team.

Individual fundings can be acquired from standard financial institutions and cooperative credit union. Here are some bottom lines to take into consideration. Credit score cards can provide a versatile way to obtain money for really temporary durations. Nonetheless, borrowing money on a debt card is usually extremely expensive with yearly percentage rates of passion (APR) frequently getting to 20% to 30% or even more a year.

{kind=link}

Latest Posts

Can Self-banking System protect me in an economic downturn?

Privatized Banking System

How do I optimize my cash flow with Wealth Management With Infinite Banking?